April 2026 Net Worth Update: $2.24M — Up $43K Despite $11K Month

YNAB says I spent ~$11.7K in April. ProjectionLab says my net worth went up $43K. Both are right.

That gap is what I want to walk through. Most of the ~$11.7K is travel I'd already accounted for at the year level — the rest of the budget held at its usual shape. Net worth: $2.24M. Up $43K from March.

TL;DR:

- Total Net Worth: $2.24M (up $43K from $2.197M)

- Key Driver: RSU vest (~$22K gross, ~$8.6K net shares) + two paychecks of automatic contributions

- Spending: ~$11.7K — most of it planned travel; core budget held at ~$5.6K

- FI Progress: 44.8% toward $5M

The Bottom Line

| Metric | Value | Change |

|---|---|---|

| Assets | $2.59M | +$43K |

| Liabilities | $346.5K | -$0.9K |

| Total Net Worth | $2.24M | +$43K |

All-time net worth trend. Up $642.1K (40.21%) since ProjectionLab started tracking.

| Month | Net Worth | Growth | New Money In | Market Did |

|---|---|---|---|---|

| Nov 2025 | $1.999M | +$15.1K | $5.8K | $9.4K |

| Dec 2025 | $2.042M | +$42.5K | $6.1K | $36.4K |

| Jan 2026 | $2.080M | +$38.6K | $24.0K | $14.6K |

| Feb 2026 | $2.134M | +$53.8K | $18.2K | $35.6K |

| Mar 2026 | $2.197M | +$54.0K | $27K | $27K |

| Apr 2026 | $2.240M | +$43K | $9K | $34K |

Six months, $241K of growth — about +12% from where I started, roughly a 24% annualized pace. Across those six months, markets contributed ~$157K vs ~$90K of new money — markets are doing about 65% of the work. That's the quiet shape of compounding at this NW level: contributions still matter, but they're no longer the dominant lever.

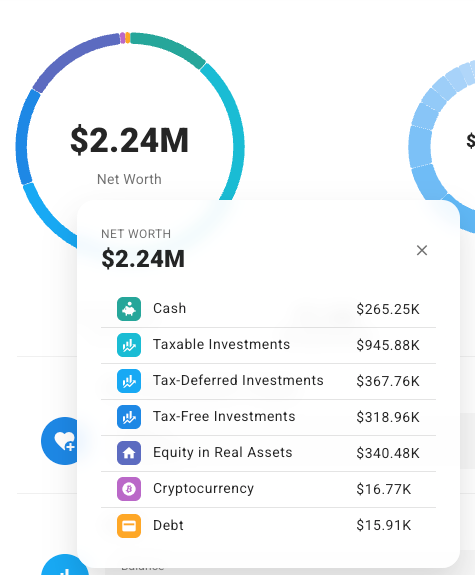

Assets Breakdown: $2.59M

| Asset Class | Value |

|---|---|

| Taxable Brokerage | $945.9K |

| Retirement Accounts | $686.7K |

| Real Estate & Business | $671.1K gross / $340.5K equity |

| Cash & Equivalents | $265.3K |

| Crypto | $16.8K |

Assets, liabilities, and equity breakdown as of early May 2026.

Taxable brokerage crossed $945K — M1 at $493K, Schwab at $202K, Schwab Robo at $116K. Retirement accounts hit $686.7K combined (401k $368K + Roth 401k $206K + HSA $76K + Roth IRA $36K). The tax-free bucket quietly crossed $319K.

Cash dropped slightly to $265K. The February bonus is still parked in money market (SNSXX, $235K). Probably the most expensive non-decision I'm making.

Liabilities: $346.5K

Same story as every month.

- Mortgage: $330.6K — down another ~$800.

- M1 Loan: $15.9K — slowly shrinking.

- Credit Cards: $0 — paid in full.

Paychecks and RSU

Two April paychecks: ~$9.6K gross each, ~$1.7K take-home each. Same ~$9.6K-to-$1.7K-cash mechanics I broke down in detail last month — most of the gross is going into 401k, Mega Backdoor, HSA, and ESPP before it ever reaches checking.

YTD Front-Loading

| Account | YTD | 2026 Limit | % Done |

|---|---|---|---|

| 401k Pre-Tax | $11.5K | $24,500 | 47% |

| Mega Backdoor Roth | $18.0K | ~$46,500 | 39% |

| HSA (Emp + Employer) | $3.0K | $8,750 | 35% |

| ESPP | $19.0K | $21,500 | 88% |

ESPP capped out in May at ~$21.5K — that's the effective post-tax contribution limit, not the IRS $25K stock-purchase cap. The ~$2.4K/paycheck that has been going into ESPP is already coming back as take-home cash — about $5K/month — for the rest of the year. That's a decision I haven't made yet.

RSU Vest

Four tranches hit the same day: ~$22K gross. About $13.7K withheld in shares for taxes. Net: ~$8.6K of company stock landed in the brokerage.

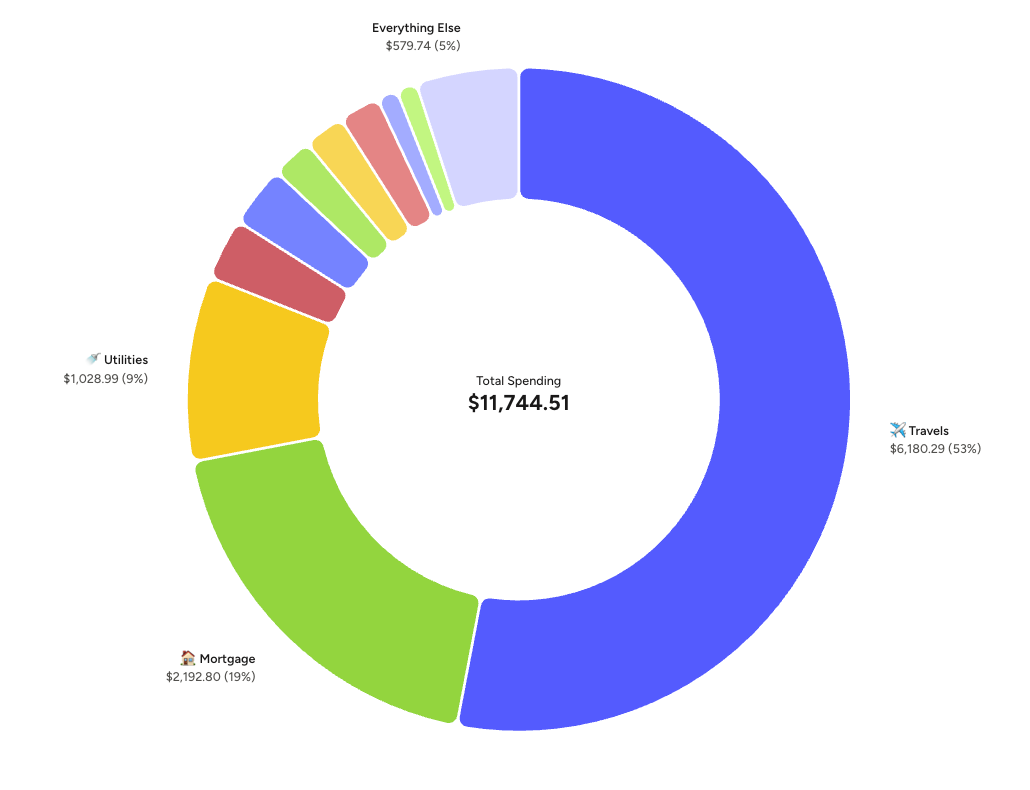

Spending: ~$11.7K

April spending. Travel dominated the donut; the rest of the budget held.

Strip out travel and April spending was ~$5.6K — within rounding of my $5K target. The $6.2K travel line is part of a $10K annual budget that lands across three calendar months (Feb booking, April trip, May CC tail) — planned, not creep.

| Category | Amount | % of core |

|---|---|---|

| Mortgage | $2.2K | 39% |

| Everything else (groceries, dining, fitness, etc.) | $2.3K | 42% |

| Utilities | $1.0K | 18% |

| Core total | $5.6K | 100% |

Mortgage is fixed. Utilities are a narrow range. The "everything else" bucket — groceries, dining, fitness — is where I have actual discretion, and it held its usual shape.

Reflections

-

The $235K cash position is more deliberate than it looks. I keep framing it as a "non-decision," but the honest version is: I'm holding it as a sequence-of-returns hedge. If markets drop sharply in the next year or two, I'd rather have ammunition to buy than be forced to ride it down with everything fully allocated. The opportunity cost is real — $235K earning ~4% in MM vs an after-tax ~7% expected in equities is roughly ~$7K/year I'm forfeiting. That's the price of optionality, and right now I'm willing to pay it. The real tension isn't whether to deploy — it's how much of this is a genuine hedge and how much is just me avoiding the decision.

-

ESPP just capped in May. ~$5K/month is coming back as cash. Decided. M1 margin loan paydown first — about three months to clear the $15.9K balance — then $5K/month DCA into taxable ETFs through year-end. Guaranteed return at the margin rate beats parking in MM, and tranching the rest addresses the valuation caution without sitting in cash.

-

44.8% there. Six months in, ~$240K added since crossing $2M last October.

Next up: setting up the ESPP-paydown-then-DCA automation, and watching whether the cash hedge thesis still feels right next month.

Your turn. $235K in money market as a sequence-of-returns hedge — am I being prudent, or rationalizing inaction? If you've thought about SoRR for your own FIRE plan, where do you draw the line between "real hedge" and "expensive comfort blanket"? Drop a comment.

Join the Quest

This blog is my public commitment to the grind from $2M to $5M. If you're a high earner tired of the corporate hamster wheel and want to see the real numbers behind the exit, subscribe and follow along. Let's figure this out together.

Member discussion