March 2026 Net Worth Update: $2.2M, a $10K Tax Refund, and Small-Business Arbitrage

Filed my 2025 taxes a couple weeks ago. Got about $10K back in federal refund.

Not because I got unlucky with withholding. Because owning a small business lets me legally deduct real costs — initial investment, operating expenses — against my W-2 income. That's the tax arbitrage I didn't know existed until I started doing it.

We'll break the mechanics down below. First, here's what March looked like.

Quick TL;DR:

- Total Net Worth: $2.2M (up $63K; +$54K apples-to-apples after an ESPP accounting fix)

- Tax Refund: ~$10K federal, byproduct of small-business deductions stacking on W-2 income

- Spending: $6,218 — down $2.3K from February. Back on the glidepath.

- FI Progress: 43.9% toward my $5M goal (crossed $2M last October)

A quick note on dates. I'm writing this in mid-April, so the numbers include a recent RSU vest and the first April paycheck. Call it a March-wrap plus mid-April check-in. Getting the post out beats being a purist about month boundaries.

The Bottom Line

| Metric | Value | Change |

|---|---|---|

| Assets | $2.54M | +$67K |

| Liabilities | $347.4K | -$1.5K |

| Total Net Worth | $2.2M | +$63K |

All-time net worth trend. Up $598.7K (37.49%) since I started tracking.

Quick housekeeping. I caught an accounting gap this month. My ESPP contributions sit in a holding account until each purchase window closes, and Empower doesn't track that balance. I'd been leaving it off my net worth for months. Fixing it this time: $16.6K YTD going in. About $9K of that headline +$63K is the methodology catch-up — true apples-to-apples growth vs Feb is closer to +$54K.

Either way, the machine is working.

| Month | Net Worth | Growth | New Money In | Market Did |

|---|---|---|---|---|

| Nov 2025 | $1.999M | +$15.1K | $5.8K | $9.4K |

| Dec 2025 | $2.042M | +$42.5K | $6.1K | $36.4K |

| Jan 2026 | $2.080M | +$38.6K | $24.0K | $14.6K |

| Feb 2026 | $2.134M | +$53.8K | $18.2K | $35.6K |

| Mar 2026 | $2.197M | +$54.0K | $27K | $27K |

Five months, $200K of growth. The trend is what I modeled in Projection Lab last year — and mostly, it's holding up.

Assets Breakdown: $2.54M

| Asset Class | Value |

|---|---|

| Taxable Brokerage | $932.6K |

| Retirement Accounts | $663.9K |

| Real Estate & Business | $339.7K |

| Cash & Equivalents | $259.7K |

| Crypto | $16.0K |

Net worth, assets, liabilities, and real-asset equity at a glance.

Retirement accounts went from $645.1K to $663.9K — $18.8K added in a single month with no bonus behind it. Pure paycheck deductions compounding. Taxable brokerage crossed $900K for the first time ($932.6K with the ESPP holding line added back).

Cash is still parked at $259.7K. Some of that bonus from February is waiting for a decision. Probably money market for now, maybe tax-loss harvesting targets later in the year.

Liabilities: $347.4K

Same as always.

- Mortgage: $331.4K — ticking down slowly.

- M1 Loan: $16.0K — paying down in the background.

- Credit Cards: $0 — paid in full, like every month.

The $1,700 Paycheck: Why My Take-Home Looks Small

Opened a recent paystub. Gross: ~$9.6K. Take-home: ~$1.7K.

That's not a typo. $9.6K gross, $1.7K in the bank.

Where did it all go? Roughly $800 to 401k. $1.2K to Mega Backdoor. $260 to HSA. $2.4K to ESPP. The rest to taxes. By the time payroll finished pulling levers, there was basically nothing left to spend. Which sounds bad — until you realize that's the system working exactly as designed. (I wrote about why this setup matters in Max Contribution to 401k and Mega Backdoor Roth in 2026.)

YTD Front-Loading (through mid-April)

| Account | YTD | 2026 Limit | % Done |

|---|---|---|---|

| 401k Pre-Tax | ~$10.7K | $23,500 | ~46% |

| Mega Backdoor Roth | ~$16.9K | ~$46,500 | ~36% |

| HSA (Emp + Employer) | ~$2.7K | $8,550 | ~32% |

| ESPP | ~$16.6K | $25,000 | ~66% |

ESPP is way ahead of pace — on track to max by early summer. Everything else is tracking to year-end, which is what I wanted when I scrapped the aggressive Q1 front-loading plan back in February. Slower, but I don't lose employer match on the tail of the year.

Oh, and I had a regular RSU vest this week — roughly $22K gross. About half got withheld via share sale for taxes, the rest landed in the brokerage as new stock. Zero cash changed hands. Normal RSU cadence, not a windfall.

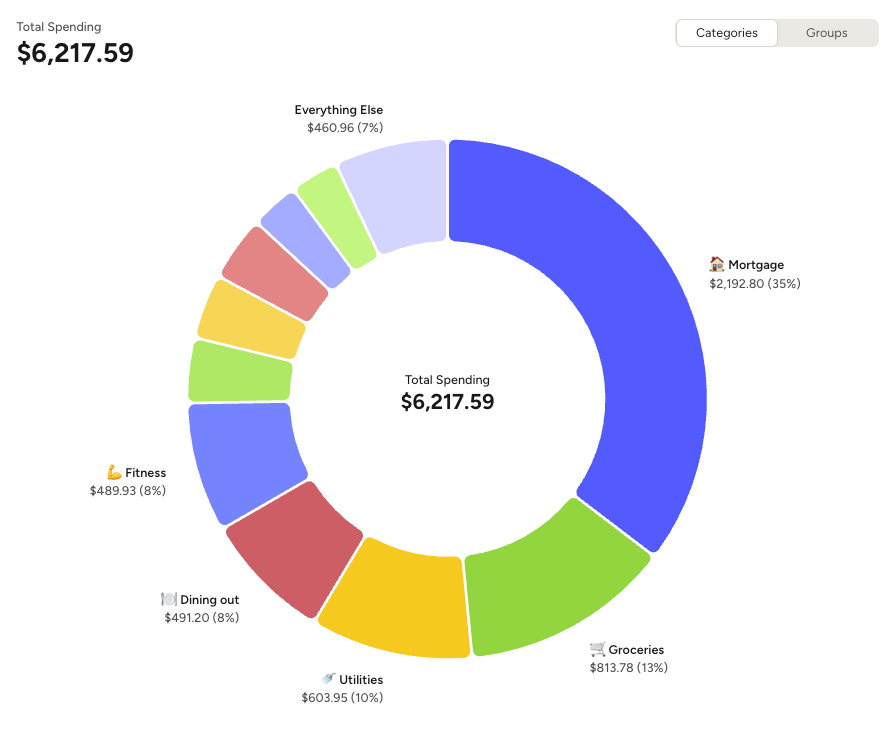

Spending: $6,218

March spending. Mortgage dominates; no travel spike this month.

Big improvement from February's $8.6K. Still over my $5K stretch target, but the gap narrowed.

What dropped? Travel — $1,835 in Feb, $0 this month. That April trip was already paid for.

What held steady? Fitness at $490 (shoes, gear, race entries). Groceries at $814, down from $1.2K — meal prep is sticking. And dining out showed up at $491; worth watching.

Still looking for about $1,200 to trim to get inside $5K. Not making dramatic cuts. Just paying attention to where it's going.

The $10K Refund: Tax Arbitrage Through a Small Business

Back to the opener.

People hear "tax refund" and think "yay, found money." It's not found money. It's money I overpaid that the government finally sent back. What makes mine interesting isn't the refund itself — it's why I overpaid.

A couple years ago I bought into a small business (the $80K line in my assets). That wasn't just a wealth-building asset. It reshaped my tax situation entirely.

Here's the basic math most W-2 employees never see:

- Depreciation on the business's assets: The equipment, build-out, and other qualifying property the business acquired with my capital became depreciable over several years. That depreciation flows through to my 1040 as a real deduction against ordinary income. The IRS allows accelerated write-offs via Section 179, plus bonus depreciation on top (currently phasing down — 20% in 2026, zero in 2027 unless Congress extends).

- Operational costs: Ordinary and necessary business expenses — rent, software, contractor payments, travel, even a portion of home-office costs — offset business revenue. If the business runs lean or slightly negative on paper, that loss flows through and reduces my W-2 taxable income.

- Net effect: My taxable income on paper ends up lower than my actual cash earnings. My W-2 withholding stays tuned to my gross. Come April, the IRS hands the difference back.

That's the arbitrage. Nothing hidden, nothing shady. Just using the tax code the way it's written, where business owners get treated differently than pure W-2 earners.

Two real constraints worth knowing if you're thinking about replicating this: you need to materially participate in the business for losses to offset W-2 income (passive investors can't), and chronic paper losses invite IRS hobby-loss scrutiny. This works because there's a real business here with a real profit motive — not a structure invented to generate paper losses.

This isn't a step-by-step guide — every situation is different, entity structure matters (LLC vs. S-Corp vs. sole prop), and I'm not your accountant. But the takeaway is worth internalizing: if you're a high-W-2 earner, owning something — a rental, a small business, a side venture with real deductible costs — changes your effective tax rate in ways no amount of 401k maxing can match.

The $10K is a one-month bump. The structure keeps paying as long as the business is alive. That's why this matters more than any single month's growth line.

Reflections

- Owning something changes the math. A small business doesn't just build equity — it rewrites your tax situation. The $10K refund is the annual receipt for that structural choice.

- Quiet months are the engine. No bonus, no market drama, just autopilot — and still $54K of growth. The boring months are where the compounding happens.

- A $1,700 take-home paycheck is a feature, not a bug. If my paycheck looks small, it's because I've aimed every lever at tax-advantaged compounding. Small checks now, real options later — the same logic behind the 2026 One-Page Financial Plan I'm running against.

- Track honestly. Found my ESPP methodology gap this month and fixed it. I'd rather show a less-flattering number than fool myself with bad math.

Next up: April spending, figuring out what to do with the $259K in cash, and putting that refund to work.

Your turn. Are you running a W-2 + side-business setup? What structures are working for you (LLC, S-Corp, something else)? Drop a comment or reply to this email — I'm genuinely curious what the pattern looks like for others at this income level.

Join the Quest

This blog is my public commitment to the grind from $2M to $5M. If you're a high earner tired of the corporate hamster wheel and want to see the real numbers behind the exit, subscribe and follow along. Let's figure this out together.

Member discussion