February 2026 Net Worth Update: $54K Growth and a Bonus Well Spent

So my annual bonus hit. $54k gross.

Now — I could've let that sit in checking and feel like a baller for a couple weeks. But nah. $4,884 went straight into the 401k, another $6,511 into my Mega Backdoor Roth, and honestly, taxes ate most of the rest. Between that bonus and the regular paycheck deductions, $18,193 landed in tax-advantaged accounts this month alone.

The result? Net worth jumped $53.8K. Best month I've had since I started this whole thing.

Quick TL;DR:

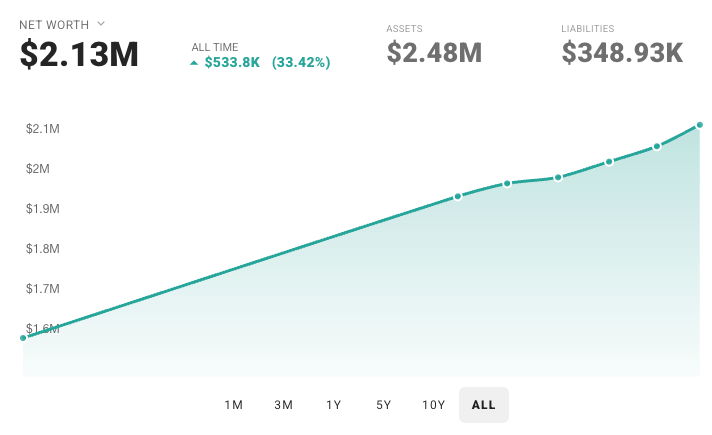

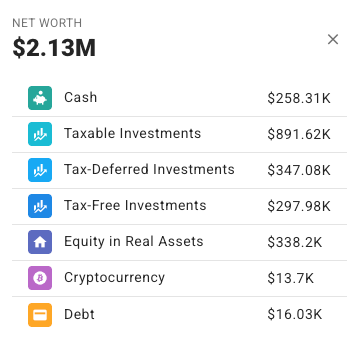

- Total Net Worth: $2.13M (up $53.8K from last month)

- Key Driver: Annual bonus + paycheck deductions = $18.2K invested before I could touch it

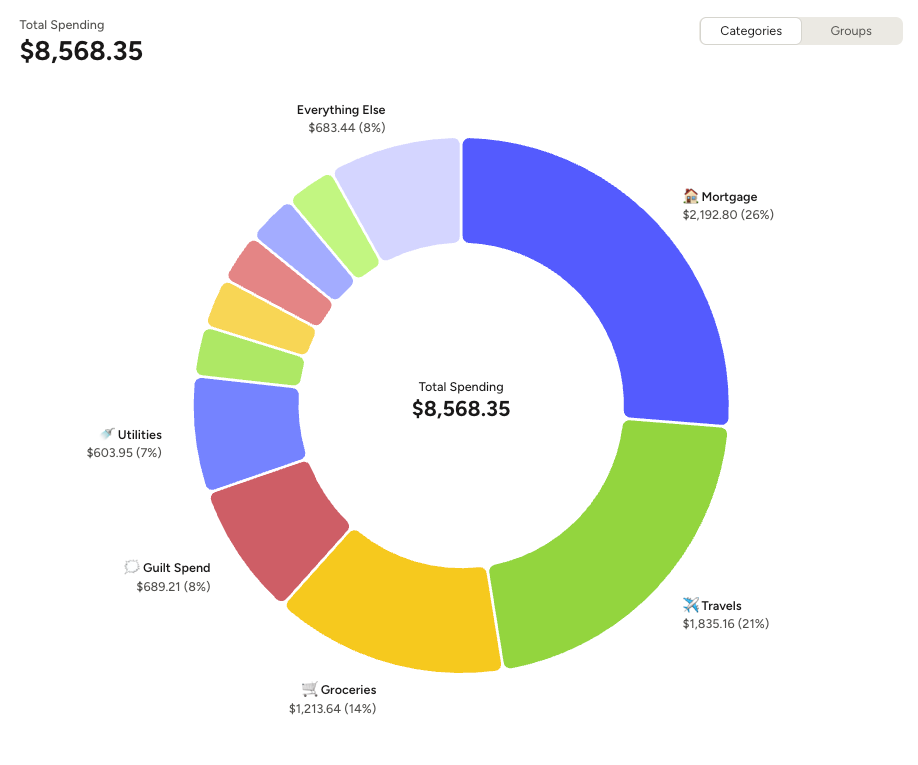

- Spending: $8,568 (includes $1,835 in planned travel — strip that out and I'm basically on target)

- FI Progress: 42.6% toward my $5M goal

The Bottom Line

| Metric | Value | Change |

|---|---|---|

| Assets | $2.48M | +$54.5K |

| Liabilities | $348.9K | -$0.7K |

| Total Net Worth | $2.13M | +$53.8K |

$53.8K in a single month — up 2.59%. Here's how the journey has looked since I started tracking:

| Month | Net Worth | Growth | New Money In | Market Did |

|---|---|---|---|---|

| Nov 2025 | $1.999M | +$15.1K | $5.8K | $9.4K |

| Dec 2025 | $2.042M | +$42.5K | $6.1K | $36.4K |

| Jan 2026 | $2.080M | +$38.6K | $24.0K | $14.6K |

| Feb 2026 | $2.134M | +$53.8K | $18.2K | $35.6K |

Four months, $150K in growth. My money is starting to work harder than I do — February's market contribution ($35.6K) was nearly double what I put in ($18.2K). That's the compounding kicking in.

All-time: $2.13M

Assets Breakdown: $2.48M

| Asset Class | Value |

|---|---|

| Taxable Brokerage | $891.6K |

| Retirement Accounts | $645.1K |

| Real Estate & Business | $338.2K |

| Cash & Equivalents | $258.3K |

| Crypto | $13.7K |

February snapshot from Empower.

Retirement accounts went from $615.7K to $645.1K. That's $30K in two months just from front-loading. Love seeing that number climb. Cash is sitting at $258K — some of the bonus is parked in checking while I think about where to put it next.

Liabilities: $348.9K

Same story as always. Autopilot.

- Mortgage: $332.9K — ticking down slowly.

- M1 Loan: $16K — almost done with this one, finally.

- Credit Cards: $0 — paid in full, like every month.

Income & Spending: Bonus Month

February gross was $73,395. Wild number. But the vast majority of it went exactly where I planned.

Where the Money Went

| Deduction | Amount |

|---|---|

| 401k (Pre-Tax) | $6,487 |

| Mega Backdoor Roth | $8,777 |

| HSA | $522 |

| ESPP | $2,406 |

| Total from Paychecks | $18,193 |

Made a couple tactical calls this month worth mentioning.

I paused ESPP temporarily. Why? Because I didn't want the bonus to get swallowed by stock purchases before I even saw the cash. That's back on now — plan is to max it by June.

Also shifted my 401k approach. Was originally trying to max it by end of Q1, but I realized I'd lose employer match on the back half of the year if I did that. So now I'm spacing it out. Less flashy, more practical. Getting free money every paycheck beats bragging about front-loading speed.

Spending: $8,568

Alright, let's talk about this number. Looks big. Context helps.

February spending. That 21% travel slice? Planned trip in April. Not a surprise.

$1,835 of that was travel — booked a week-long trip for April. My yearly travel budget is $10K, so this was always in the cards. Just happens to show up on February's ledger. Take that out and I'm at $6,733. That's maybe $1,700 over the $5K target? On a $2.13M net worth... I'm not losing sleep over it.

Rest of it was pretty intentional. $689 on running shoes and workout gear — I've been going hard on fitness lately and honestly, $2.13M felt like a good moment to invest in myself a bit. Groceries landed at $1,214, which is actually down from January's $1,313. The meal prep thing is genuinely sticking.

Reflections

- Bonuses are wealth-building events. $54K gross, $11.4K into retirement accounts from a single check. One payroll event moved the needle more than most regular months combined.

- Good plans evolve. Pausing ESPP, spreading out 401k — neither was in the original playbook. But protecting cash flow while still capturing every dollar of employer match? That's just common sense.

- Spend on what matters to you. Travel and fitness aren't "waste." The whole point of this journey is building a life worth living right now, not just at some distant finish line.

Tax season is next. And then I've got an April trip on the calendar to look forward to.

Join the Quest

This blog is my public commitment to the grind from $2M to $5M. If you're a high earner tired of the corporate hamster wheel and want to see the real numbers behind the exit, subscribe and follow along. Let's figure this out together.

Member discussion