Healthcare in Early Retirement: How to Plan When You’re Too Young for Medicare

Most people stay in their jobs for "One More Year" solely because of health insurance. It's a constraint that feels impossible to unlock.

The fear is rational. The "sticker shock" number for a family of four is high: roughly $2,500 a month, or $30,000 a year. That’s a significant expense every single year, just for the privilege of financial protection against medical bankruptcy.

But here is the reality: You don't have to pay that much.

In the Chubby FIRE world (Net Worth $4M - $5M), we have a unique advantage. We have the assets to pay the full price if necessary—which removes the catastrophic risk—but we also have the flexibility to optimize our income to pay a fraction of that cost.

Healthcare in early retirement is solvable. It requires either money or strategy. We have the first, so we can choose to use the second.

TL;DR

- Use the ACA Marketplace because it guarantees coverage for pre-existing conditions and caps premiums based on income.

- For a couple spending $150,000/year, a high-quality Gold plan costs roughly $7,300 to $15,150 depending on tax optimization (based on KFF 2025 subsidy estimates + average Gold upgrade costs).

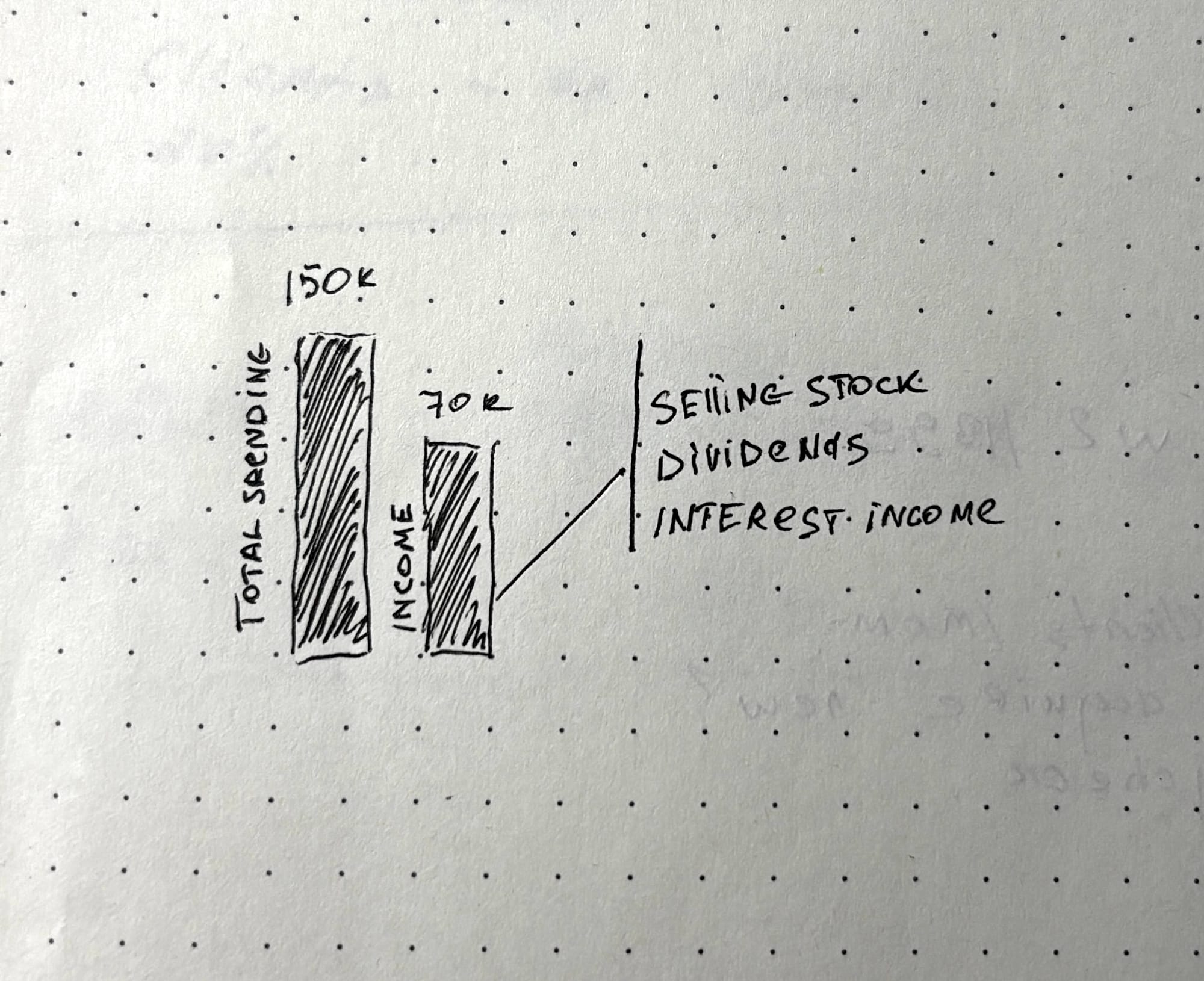

- Subsidies are based on MAGI (Reported Income), not Spending. You can spend $150k while reporting $70k income to the IRS to drastically lower your premiums.

The Landscape: What Do Early Retirees Do for Health Insurance?

When you leave your employer, you lose the group plan subsidized by HR. You are now in the wild. Here is the menu of actual options for 2025/2026.

1. The ACA Marketplace (The Gold Standard)

This is Plan A. The Affordable Care Act (ACA), also known as Obamacare, created online marketplaces where private insurers compete for your business, and the government provides tax credits to lower costs based on your income.

- How to Apply: Go to HealthCare.gov. Enter your zip code. It will either let you apply there or redirect you to your state's specific exchange (like CoveredCA or NY State of Health).

- Crucial Detail: When the application asks for your income, it wants your estimated income for the year you are applying FOR, not the tax return you just filed. If you retire in 2025 and apply for 2026 coverage, you enter your projected (low) 2026 income, which unlocks the subsidies immediately.

- Pros: They are "real" insurance. They cover pre-existing conditions, preventive care is free, and there are no lifetime limits.

- Cons: The unsubsidized price is high ($2k-$3k/mo). Networks can be narrower than your corporate PPO.

- Verdict: This is what most of us will use.

2. Spouse's Plan (The Spousal Advantage)

If one partner is still working, you are in a strong position. It is almost always cheaper and better to hop onto a spouse's employer plan than to buy private insurance. If your spouse plans to continue working, this solves the entire problem.

3. COBRA (The Bridge)

COBRA is a federal law that lets you keep your exact current employer group plan for 18 months after you quit. It is the same network, same doctors, same coverage.

- How to Get It: You don't apply online. Your employer's benefits administrator will mail you a "COBRA Election Packet" within 14-45 days of your last day. You fill out the form and mail it back with a check.

- The Catch: You pay the entire premium (your share + the employer's share) plus a 2% admin fee.

- When to use it: It’s perfect for your "Transition Year" (Year 1).

- Why? If you retire in June, your income for that year will be high (salary + bonus), so you won't qualify for ACA subsidies anyway.

- Strategy: Stick with COBRA through December 31st to keep your deductible credits and doctors. Then, switch to ACA for January 1st of Year 2 when your income drops and subsidies kick in.

What We Avoid

I avoid the following options. We are "Chubby FIRE," not "Barista FIRE." The goal is to retire and own our time, not to trade 20 hours a week to save on premiums.

- Part-Time / "Barista FIRE": Working at Starbucks or REI for benefits. Hard pass. I didn't build a multimillion-dollar portfolio to go back to a scheduled shift.

- Health Sharing Ministries: They are not insurance; they are "voluntary sharing" programs. There are no legal guarantees they will pay your bills. With a $3M+ net worth, you are protecting a legacy. Saving $500/mo isn't worth risking a denied cancer claim that wipes out your portfolio.

The Mechanics of Costs & Subsidies

The key mechanism is this: Health insurance cost is based on your INCOME, not your WEALTH.

The Affordable Care Act (ACA) offers subsidies (Premium Tax Credits) that cap your insurance premiums as a percentage of your income. As of late 2025, provided the Inflation Reduction Act subsidies are extended, you won't pay more than ~8.5% of your income for a benchmark Silver plan.

You can plug your own numbers into the KFF Subsidy Calculator to see exactly how much the government will pay toward your premiums.

The distinction: MAGI vs. Spending

The government doesn't care that you spend $150,000 a year. They care about your Modified Adjusted Gross Income (MAGI).

Spending $150k but reporting $70k income: The key to subsidies.

- Spending from Cash Savings: $0 Income.

- Selling Stock: Only the gain is income. If you sell $100k of stock with an $80k cost basis, your income is only $20k.

- Roth IRA Withdrawals: $0 Income.

Critical Note on Timing: Subsidies are based on your estimated income for the upcoming coverage year, not your past tax return. When you apply in Nov 2025 for 2026 coverage, you tell them: "I am retired, my 2026 income will be $60k." They grant the subsidy based on that estimate—you don't have to wait a year for your tax return to "show" low income.

The Example

Let's say you are a family of four in a high-cost city.

- Actual Spending: $140,000 / year.

- Reported MAGI: $70,000 (via strategic withdrawals).

- The Result: instead of paying the "Scary Number" of $2,500/mo, you might pay ~$400/mo for a high-quality plan.

You don't need to be poor to get cheap health insurance; you just need to be tax-efficient.

The Execution Framework: A Year-by-Year Plan

Here is how to structure your move from corporate benefits to early retirement healthcare.

Phase 1: Pre-Launch (1 Year Out)

- The "Body Audit": While you still have excellent employer coverage, do everything. Get the MRI for that knee, get the dental crown, refill all prescriptions, do physical therapy. Maximize the benefits you are currently paying for.

- Build the "Cash Bridge": Save 1-2 years of living expenses in cash or high-basis taxable brokerage accounts. This gives you the "fuel" to keep your MAGI artificially low in your first years of retirement without starving.

Phase 2: The Transition (Year 1)

- The Trigger: Leaving your job is a "Qualifying Life Event." This triggers a Special Enrollment Period, meaning you can buy ACA insurance immediately—you don't have to wait for November Open Enrollment.

- The COBRA Strategy: You have 60 days to retroactively elect COBRA. If you leave your job on November 1st, you technically don't have to buy insurance for Nov/Dec. If you have a medical emergency, you sign the COBRA paperwork in the hospital and pay the premium. If you stay healthy, you save two months of premiums. (Consult a pro before trying this!).

Phase 3: Steady State (Year 2+)

- The "Chubby" Upgrade: Since we aren't trying to survive on $40k a year ("Lean FIRE"), we can use the subsidies differently. Instead of using them to get a free Bronze plan with a huge deductible, use the subsidy to buy a Gold or Platinum PPO.

| Feature | Lean FIRE Strategy | Chubby FIRE Strategy |

|---|---|---|

| Monthly Premium | $0 after subsidy | ~$600 after subsidy |

| Deductible | High ~$7,500 | Low ~$1,000 |

| Network Access | Narrow HMO | Broad PPO |

| Peace of Mind | Low | High |

Table: Comparison of Lean FIRE (Bronze) vs. Chubby FIRE (Gold) strategies.

- The Philosophy: We are getting older. Health is our #1 asset. I'd rather pay $600/mo for excellent access and a broad network than $0/mo for a plan where I can't find a doctor.

Legislative Watch: The 2026 Cliff

Last Updated: November 2025

The enhanced subsidies (the 8.5% income cap) are currently set to expire on December 31, 2025.

- The Risk: If Congress does not extend the Inflation Reduction Act subsidies, the "subsidy cliff" returns in 2026. If your income is even $1 over 400% of the Federal Poverty Level, you lose all subsidies. Check current FPL tables here.

- The Strategy: This makes the "Cash Bridge" (Phase 1) even more critical. If the cliff returns, you will need to suppress your MAGI strictly below 400% FPL to get any help.

- The Chubby Backstop: If the law changes and we lose subsidies entirely, we revert to paying the full market rate. It increases our expense line, but it does not break the portfolio.

I will update this section as 2026 legislation is finalized.

Conclusion: It's Just a Line Item

The fear of the $30,000 healthcare bill keeps too many people working jobs they hate for years longer than necessary.

If subsidies exist in 2026 and beyond, great—we play the game and pay $5,000 a year.

If subsidies disappear? Fine. We pay the full $30,000.

It’s a significant cost, but on a $5M portfolio, it’s a 0.6% expense ratio. It impacts the budget, but it doesn’t kill the plan. It’s just a line item. You have the money to handle the worst case, which gives you the freedom to optimize for the best case.

Disclaimer: I am not a financial advisor, tax professional, or insurance broker. The information provided in this article is for educational and informational purposes only and should not be construed as professional financial or legal advice. Healthcare laws, tax codes, and subsidy calculations change frequently. Please consult with a qualified professional before making any financial or healthcare decisions.

Member discussion