January 2026 Net Worth Update: I Spent More Than I Made (On Purpose)

This month, I technically spent more than I made.

My checking account saw $3,802 in deposits. My spending was $6,007.

In a normal world, that's a problem. In my world, that's the plan.

January was the start of my aggressive front-loading strategy for 2026. I diverted nearly every available dollar into tax-advantaged accounts—401k, Mega Backdoor Roth, HSA—before it even hit my bank account. The result? A cash flow crunch on paper, but a $24K injection into my net worth.

Here's the breakdown of a month where I felt "broke" but actually got richer.

Quick TL;DR:

- Total Net Worth: $2.08M (up $38.6K from last month)

- Key Driver: Front-loading retirement accounts + RSU vesting = $24K invested in one month

- Spending: $6,007 (over my $5K target, but for a good reason)

- FI Progress: 41.6% toward my $5M goal

The Bottom Line

| Metric | Value | Change |

|---|---|---|

| Assets | $2.43M | +$32.8K |

| Liabilities | ($349.6K) | -$5.8K |

| Total Net Worth | $2.08M | +$38.6K |

I'm firmly in the $2M club now. Growth this month was a mix of raw savings ($24K in new contributions) and the market doing its thing ($14.6K in growth).

Assets Breakdown: $2.43M

| Asset Class | Value |

|---|---|

| Taxable Brokerage | $886.3K |

| Real Estate & Business | $671.1K |

| Retirement Accounts | $615.7K |

| Cash & Equivalents | $245.9K |

| Crypto | $16.2K |

Retirement accounts are up from $577K in November. That's the front-loading already paying off.

Liabilities: ($349.6K)

Nothing exciting here. Autopilot.

- Mortgage: ($333.5K) — Slowly ticking down.

- M1 Loan: (~$16K) — Almost done with this one.

- Credit Cards: $0 — Paid in full, as always.

Income & Spending: Artificial Scarcity in Action

This is the part I'm most proud of. My gross income was $52,438 (inflated by RSU vesting), but my actual take-home was only $3,802.

Where did the rest go?

| Deduction | Amount |

|---|---|

| 401k (Pre-Tax) | $1,943 |

| Mega Backdoor Roth | $4,627 |

| HSA | $783 |

| ESPP | $6,941 |

| Total from Paycheck | $14,296 |

Add the vested RSUs (net ~$9.7K), and I put over $24K into assets in 31 days.

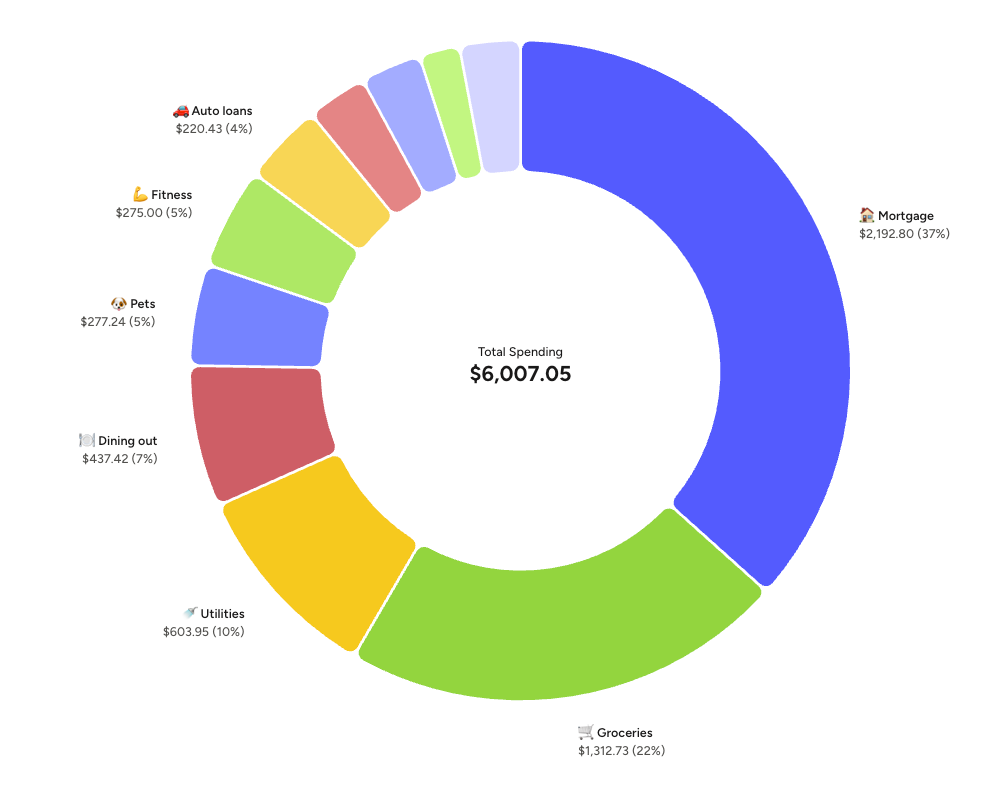

Spending: $6,007

Higher than my $5K target, and one category is to blame: groceries at $1,313.

January 2026 spending breakdown. Groceries dominated at 22%, but dining out dropped to $437.

This wasn't mindless spending though. I made a conscious shift to healthy eating and meal prepping this month. That $1,313 includes a one-time buy of glass containers and kitchen gear to support the new habit. I'm swapping dining out dollars (down to $437) for grocery dollars. I'll take that trade every time.

How I Survived the Cash Crunch

My spending ($6K) exceeded my take-home ($3.8K) by $2.2K. So where did the money come from?

My YNAB buffer. I'm currently living on money I earned 3 months ago. This buffer is what lets me front-load aggressively without panicking when the checking account looks low. It worked exactly how I planned it when I built the buffer last fall.

Reflections

- Front-loading works. Seeing small paychecks stings, but knowing I've already filled a huge chunk of my 2026 retirement buckets by January? That feels good.

- Health over convenience. The grocery bill was high, but I'd rather spend $1K at the grocery store than $1K on takeout. That's a trade I'll make every time.

- Momentum is real. At $2.08M, the day-to-day volatility doesn't rattle me like it did at $1M. There's a steadiness now that makes it easier to stay the course.

Next month: keep going. The goal is to finish maxing the 401k and Mega Backdoor Roth by end of Q1.

Join the Quest

This blog is my public commitment to the grind from $2M to $5M. If you're a high earner tired of the corporate hamster wheel and want to see the real numbers behind the exit, subscribe and follow along. Let's figure this out together.

Member discussion