June 2026 Net Worth Update: I Broke My Own Rule and Bought a $138K Sports Car

Last month I bragged about a clean balance sheet. One number, one loan, the mortgage — fixed. This month I bolted a $99K car loan onto it. On purpose.

I bought a used sports car. All-in, $138K. My net worth went down for the first time since I started writing these, to $2.24M. And I did it after spending the better part of a year telling you — and myself — that the move was to keep driving the same car and stay boring.

So let's talk about it.

TL;DR:

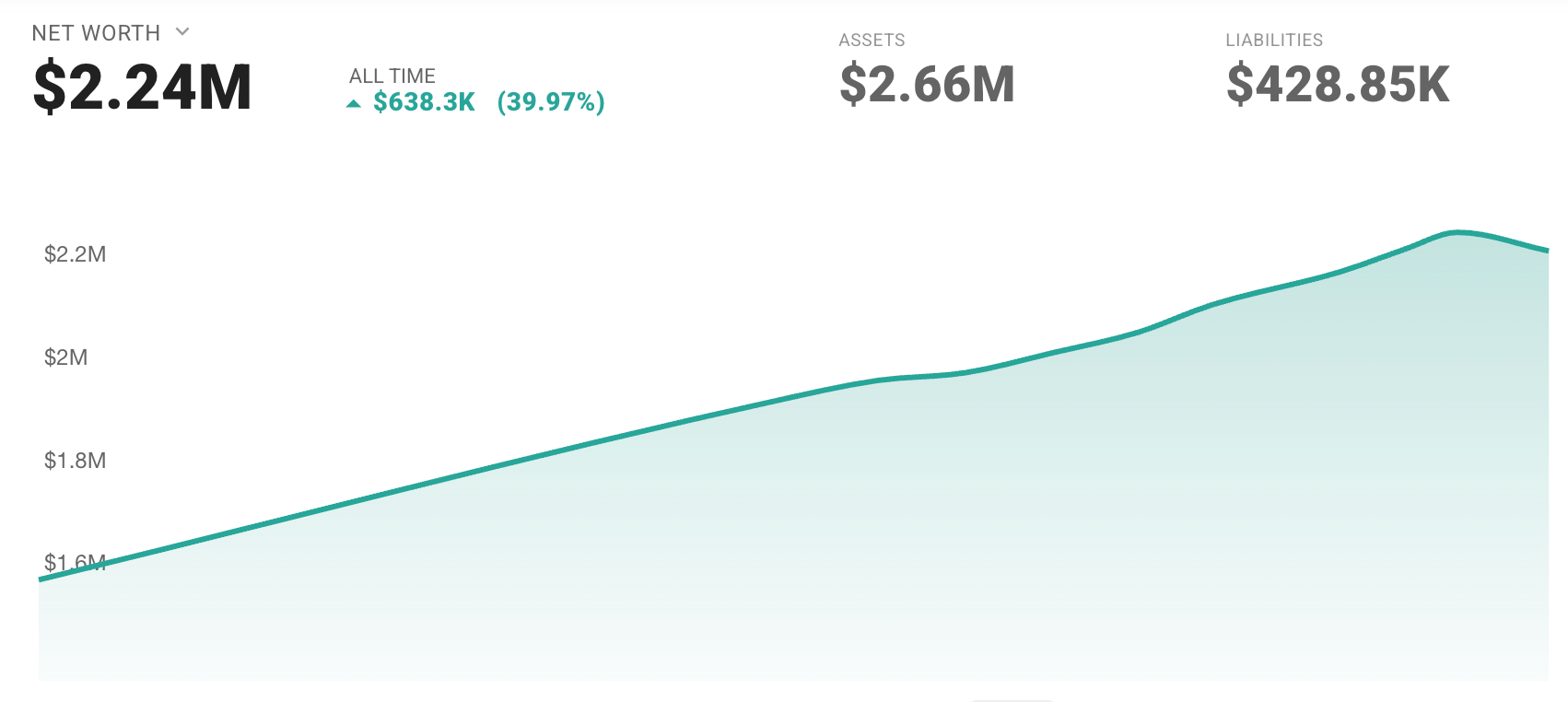

- Total Net Worth: $2.24M (down ~$35K from $2.270M)

- Key Driver: Bought a $138K sports car ($38K down, $99K financed) — a ~$25K one-time hit — into a down market (about a $20K drop)

- Spending: ~$9.5K core, plus the $38K car down payment my budget politely files under "Guilt Spend"

- FI Progress: 44.7% toward $5M (down from 45.4%)

The Bottom Line

| Metric | Value | Change |

|---|---|---|

| Assets | $2.66M | +$64K |

| Liabilities | $428.9K | +$98K |

| Total Net Worth | $2.24M | -$35K |

Net worth $2.24M. Up $638.3K (39.97%) all-time — but notice the dip at the right edge. That's June.

Assets actually rose $64K (the car added $112K); liabilities jumped $98K (the loan). The net of the two dragged net worth down.

| Month | Net Worth | Growth | New Money In | Market Did |

|---|---|---|---|---|

| Nov 2025 | $1.999M | +$15.1K | $5.8K | $9.4K |

| Dec 2025 | $2.042M | +$42.5K | $6.1K | $36.4K |

| Jan 2026 | $2.080M | +$38.6K | $24.0K | $14.6K |

| Feb 2026 | $2.134M | +$53.8K | $18.2K | $35.6K |

| Mar 2026 | $2.197M | +$54.0K | $27K | $27K |

| Apr 2026 | $2.240M | +$43K | $9K | $34K |

| May 2026 | $2.270M | +$30K | $4.5K | $25.5K |

| June 2026 | $2.235M | -$34.6K | -$14.2K | -$20.4K |

Growth = New Money In + Market Did. June's New Money In counts the car as spending: +$10.8K saved from income, minus the ~$25K net cost of the purchase ($112K asset − $99K loan − $38K down). It's the first month I've put in less than I took out.

Here's the honest split. Underneath the car I saved well — +$10.8K from income, my best in months (three paychecks, ESPP done deducting). Counting the car as spending turns that into -$14.2K. Markets separately gave back ~$20K — a real down month, not the car. Net worth fell $34.6K.

Assets Breakdown: $2.66M

| Asset Class | Value |

|---|---|

| Taxable Brokerage | $1,005.4K |

| Retirement Accounts | $715.1K |

| Real Estate & Business | $671.1K gross / $341.3K equity |

| Cash & Equivalents | $148.9K |

| Vehicle | $112.0K |

| Crypto | $11.7K |

The new line item is "Vehicle." That still feels weird to type. Cash dropped $38K — that's the down payment leaving. Taxable brokerage slipped ~$16K on the market. Retirement actually rose ~$7K, because the contributions outran the dip. Nothing dramatic anywhere except the thing with wheels.

Liabilities: $428.9K

Remember when I said this side was clean?

- Mortgage: $329.9K — down another ~$800, autopilot as always.

- Auto Loan: $99K — new. $1,883/mo at 5.25% over 60 months.

- Credit Cards: $0 — paid in full (more on that below).

I spent May celebrating the M1 payoff and a one-loan balance sheet. Six weeks later I doubled my loan count. I'm not going to pretend that isn't funny.

Paychecks and Contributions

Three paydays hit in June — a biweekly quirk that gives you an extra check twice a year. Each was ~$9.75K gross, ~$4.58K take-home, for about $13.7K in the bank. That's a fat month by design: with ESPP capped back in May, the deduction that used to eat ~$2.4K per check now shows up as cash. Convenient timing for a car down payment.

No RSU vest this month. Contributions kept marching:

YTD Front-Loading (through late June)

| Account | YTD | % of 2026 Limit |

|---|---|---|

| 401k Pre-Tax | $15.4K | 63% |

| Mega Backdoor Roth | $23.8K | 51% |

| HSA (Emp + Employer) | $4.7K | 54% |

| ESPP | $21.25K | capped |

Halfway through the year and every bucket is at or past pace. The machine doesn't care what I parked in the garage.

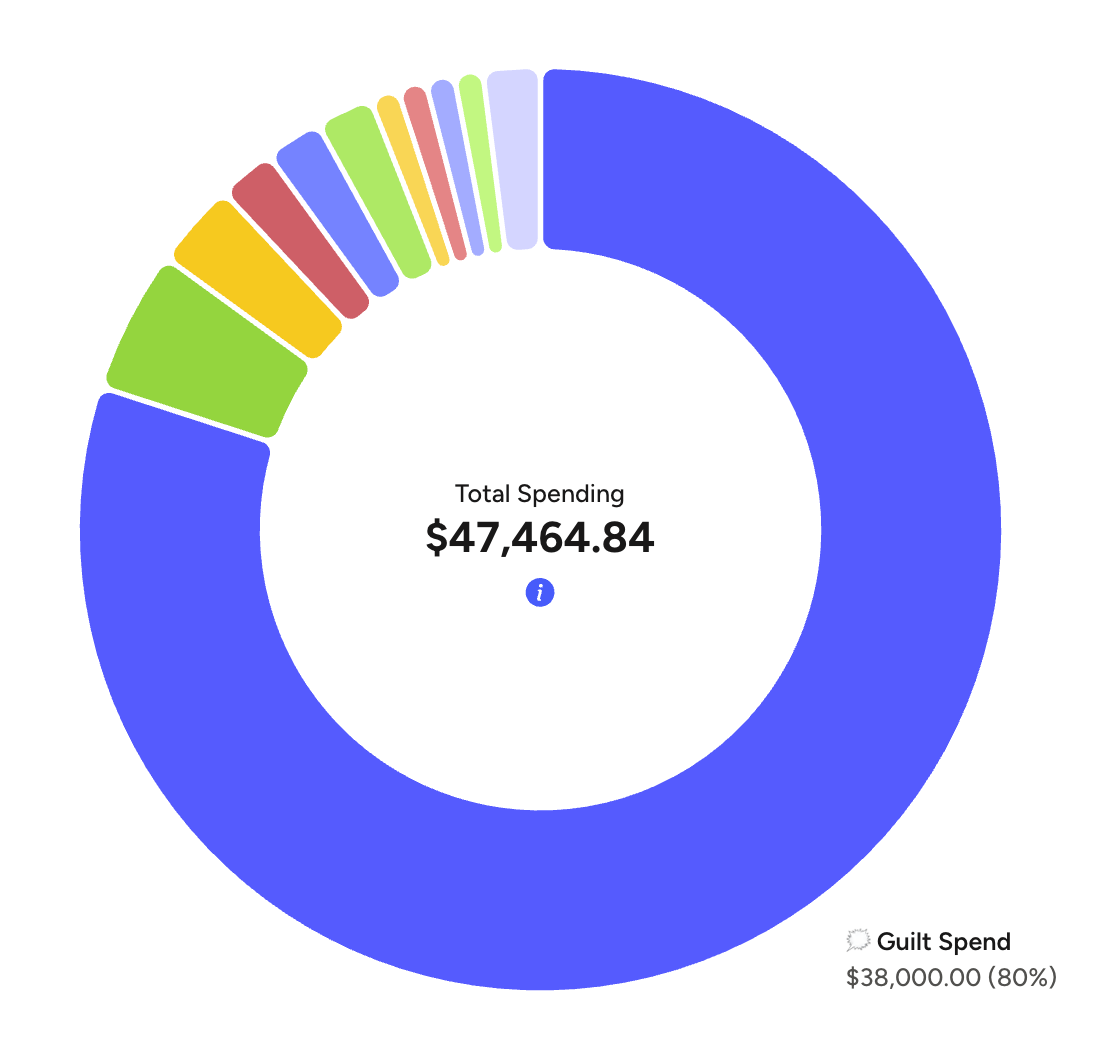

Spending: The $38K Elephant

June spending: $47,464.84. One slice is 80% of the donut. My budget labels it "Guilt Spend." I did not name that category this month — it was already there.

Total June spending was $47,464.84. Strip out the $38K car down payment and core spending was ~$9.5K — over my $5K target, driven by health ($1.5K), a gift ($1K), and $920 in bank fees I'll explain in a second. Take-home covered core easily. It did not cover a car.

Two things worth flagging: the $1,883 loan payment hasn't hit yet — first one lands in July, so next month's budget gets heavier. And that "Guilt Spend" label is real. My budgeting app has been quietly judging me for weeks.

I Broke My Own Rule

In my 2025 year in review I called a $40K car upgrade "six months of freedom lost." In the post about the real math behind my $5M target, I wrote the plan out loud: keep the condo, keep it simple, no fancy cars. Then I went and bought one for $138K.

So let me actually do the math instead of the moralizing.

The real cost isn't $138K. The car books at ~$112K today; I paid $138K all-in (MSRP $116K, the rest tax, docs, and market premium). So the net worth hit was about $25K — the down payment didn't vanish, it turned into equity. A $25K decision dressed up as a $138K one.

It's ~5% of net worth. A $112K car against $2.24M is a rounding error I chose to make — no retirement account touched, no contribution changed.

And here's the part that surprised me: the right car barely depreciates. Per the 2026 iSeeCars study, the average car sheds 41.8% of its value over five years, and even a Toyota Prius — the poster child for sensible — drops 32%. The slowest-depreciating models in the whole study are all sports cars. Mine's a 2024 with ~5K miles, so the first owner already ate the steep early drop; call it a gentle 15% from here.

The actual five-year math:

| Metric | My car (~$112K) | New Prius (~$32K) |

|---|---|---|

| 5-yr depreciation | 15% | 32% |

| Value lost | ~$16.8K | ~$10.3K |

So the "fun tax" over a sensible Prius is about $6.5K across five years — roughly $110/month — on depreciation alone. That's a shockingly small penalty. The real ongoing costs are the boring ones: premium gas where a Prius sips regular, and insurance that's a touch higher (a good credit score keeps that tame). Nothing dramatic — it just costs a bit more to feed.

The one cost I'm not pretending away: ~$80K more is tied up in a car than in a cheaper one. But I financed at 5.25% instead of liquidating investments, so the real drag is loan interest I plan to kill early — not forgone market returns.

That's the rational case. The honest one: I still wince when I check the number. But the car is genuinely, stupidly fun in a way a spreadsheet can't price. And there's a status thing I didn't expect — after years of being invisibly wealthy, I'm suddenly visibly something. People treat you differently, and I haven't decided if I like it.

The one churn that paid for itself

I also opened an Amex Platinum — my first real dip into churning. The welcome offer: 150,000 points for $12K of spend in six months. Normally that takes me half a year; this month I put the $38K down payment on the card and cleared it in one swipe. The $895 annual fee (most of June's "bank fees") stings, but 150K points for $895 is a trade I'll take. If I'm going to make an expensive decision, it may as well come with a signing bonus.

I may still kill the loan early from the money market pile — same playbook as the M1 loan; 5.25% guaranteed beats ~4% in SNSXX. But I'm in no rush.

Reflections

-

Wealth is leverage — you can upgrade your life for a small premium. I used to see a six-figure sports car and think, what an idiot, that money's on fire. I had it backwards: a car that holds its value loses barely more than a "sensible" one — you'd bleed almost the same dollars on a fast-depreciating economy car — so the upgrade costs far less than it looks. That's the quiet secret weapon of a high net worth: trade a little money for a lot of joy. You only see the lever once you can afford to pull it.

-

The scary number wasn't the real number. $138K sounds catastrophic; the actual net worth hit was ~$25K, and a well-chosen car should bleed value slowly from here. Do the math before you panic — or before you splurge.

-

A genuinely red month, isolated. Markets took ~$20K and the car took ~$25K, so net worth fell ~$35K — my first down month since I started tracking. Underneath it, income savings were my strongest in a while, +$10.8K before the car. The dip is a snapshot, not a trend.

Next up: the first $1,883 loan payment hits July, so I'll feel the real monthly bite. Then I decide whether to kill the loan, and go back to being boring. Probably.

Your turn. Where's your line between "I earned this" and "lifestyle creep"? I spent a year preaching frugality and then bought a sports car — and I can argue it both ways. If you've made a big, un-FIRE purchase on the road to financial independence, did you regret it or would you do it again? Drop a comment.

Join the Quest

This blog is my public commitment to the grind from $2M to $5M. If you're a high earner tired of the corporate hamster wheel and want to see the real numbers behind the exit — including the dumb, honest ones — subscribe and follow along. Let's figure this out together.

Member discussion