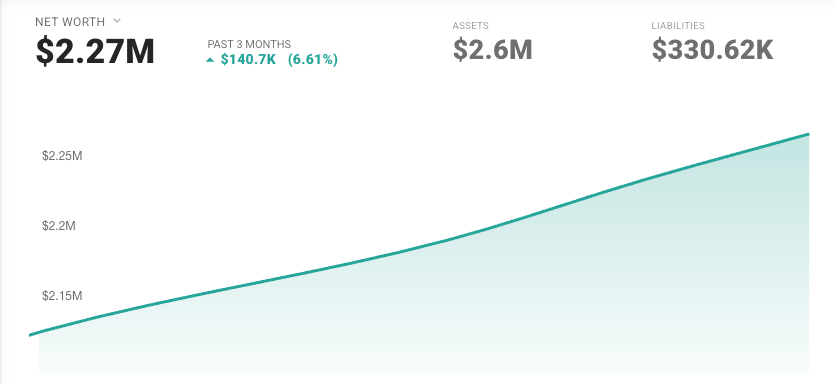

May 2026 Net Worth Update: $2.27M — M1 Cleared, Cash Deployed

Last month I called the $235K money market position "probably the most expensive non-decision I'm making." May is where I stopped making that argument.

M1 margin loan: cleared to $0. About $71K moved out of SNSXX. Allocation targets set. Net worth: $2.27M, up $30K from April.

TL;DR:

- Total Net Worth: $2.270M (up $30K from $2.240M)

- Key Driver: Markets did ~$25.5K; new contributions were slim at ~$4.5K — ESPP capped mid-month and spending was elevated

- Spending: ~$9,041 — travel again (27%), core ran a bit high at ~$6.6K

- FI Progress: 45.4% toward $5M

The Bottom Line

| Metric | Value | Change |

|---|---|---|

| Assets | $2.6M | +$15K |

| Liabilities | $330.6K | -$15.9K |

| Total Net Worth | $2.270M | +$30K |

Net worth $2.27M as of late May. Up $140.7K (6.61%) over the past three months.

| Month | Net Worth | Growth | New Money In | Market Did |

|---|---|---|---|---|

| Nov 2025 | $1.999M | +$15.1K | $5.8K | $9.4K |

| Dec 2025 | $2.042M | +$42.5K | $6.1K | $36.4K |

| Jan 2026 | $2.080M | +$38.6K | $24.0K | $14.6K |

| Feb 2026 | $2.134M | +$53.8K | $18.2K | $35.6K |

| Mar 2026 | $2.197M | +$54.0K | $27K | $27K |

| Apr 2026 | $2.240M | +$43K | $9K | $34K |

| May 2026 | $2.270M | +$30K | $4.5K | +$25.5K |

Seven months in, markets are doing about two-thirds of the work. May's new money was the lightest of the series — ESPP capped mid-month, travel spending was up, no RSU vest. Markets still delivered ~$25K. That's the quiet shape of compounding at this NW level.

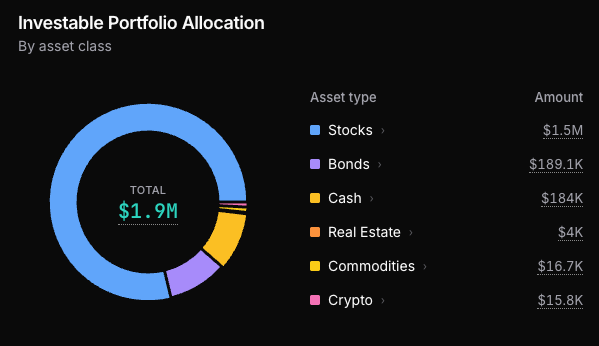

Portfolio Allocation: Putting the Cash to Work

Investable portfolio: ~$1.9M. Cash pulled down from April's elevated position after the rebalance.

April's close: the $235K money market was "probably the most expensive non-decision I'm making." The opportunity cost was real — ~4% in SNSXX versus a higher expected return in equities. I kept framing it as a hedge. In May, I moved on it.

Here's where the investable portfolio sits now:

| Asset Type | Amount | Actual | Target |

|---|---|---|---|

| Stocks | $1,500K | 79% | 80% |

| Bonds | $189.1K | 10% | 12% |

| Cash | $184K | 10% | 7% |

| Commodities | $16.7K | 1% | ~1% |

| Crypto | $15.8K | 1% | ~1% |

| Total | ~$1.9M |

What moved: ~$71K out of SNSXX. About $16K cleared the M1 margin loan first — guaranteed return beats money market, easy call. The rest — ~$44K — went into VT (Vanguard Total World Stock ETF): about $36.5K into the taxable brokerage, $7.5K maxing the backdoor Roth IRA.

The decision doc called for $5K/month DCA. I ended up closer to lump sum once I actually committed. VT closed at $158.21 as of this writing — up about 2.6% from cost basis. Two weeks. Means nothing. The point was getting it in.

Cash is still sitting at 10%, about 3 points above the 7% target. The bond allocation is light too — 10% vs 12%. So the rebalance is underway, not finished. That's fine. The direction is right.

Assets Breakdown: $2.6M

| Asset Class | Value |

|---|---|

| Taxable Brokerage | $1.021M |

| Retirement Accounts | $708.0K |

| Real Estate & Business | $671.1K gross / $340.5K equity |

| Cash & Equivalents | $187.3K |

| Crypto | $14.7K |

Taxable brokerage crossed $1M — most of the jump from April comes from the VT purchases landing in Schwab. Retirement accounts passed $700K; the tax-free bucket (Roth accounts + HSA) alone crossed $333K.

Cash dropped from $265K to $187K. That's the deployment — SNSXX pulled down from $235K to $164K. Still a buffer, now closer to the 7% target.

Liabilities: $330.6K

Same story — except M1. Gone.

- Mortgage: $330.6K — roughly flat, payment may have hit after snapshot.

- M1 Loan: $0 — paid off. Phase 1 complete, ahead of the ~3-month estimate.

- Credit Cards: $0 — paid in full.

The liability side of the balance sheet is clean now. One number. One loan. Fixed.

The Paycheck That Doubled

Two May paychecks, same ~$9.6K gross each:

| Pay Date | ESPP Deduction | Net Take-Home |

|---|---|---|

| 05/08 | $2,275.81 (final contribution) | ~$2,280 |

| 05/22 | $0 (capped) | ~$4,650 |

The 05/22 check nearly doubled in take-home — same gross, no ESPP deduction. ESPP hit its effective $21.25K contribution ceiling after the 05/08 check. From here through December, that's ~$2.4K per paycheck — roughly $5K/month — coming back as cash instead of stock purchases. I walked through the plan in April: M1 paydown first, then DCA into taxable ETFs. Phase 1 is done. Phase 2 is running.

No RSU vest in May. Separately from payroll: maxed the backdoor Roth IRA — $7.5K into VT on 05/22.

YTD Front-Loading (through 05/22)

| Account | YTD | 2026 Limit | % Done |

|---|---|---|---|

| 401k Pre-Tax | $13.1K | $24,500 | 53% |

| Mega Backdoor Roth | $20.3K | ~$46,500 | 44% |

| HSA (Emp + Employer) | $3.7K | $8,750 | 43% |

| ESPP | $21.25K | $21,250 | capped ✓ |

401k is tracking ahead of pace — 53% done with just under 5 months elapsed. MBR at 44% is right on track. HSA has a little ground to make up in the back half.

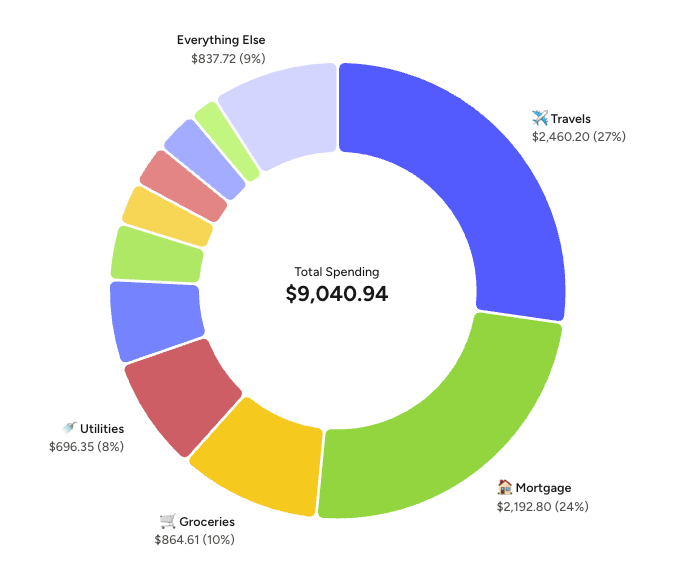

Spending: ~$9,041

May spending: $9,041. Travel led at 27%, mortgage another 24%.

| Category | Amount | % of total |

|---|---|---|

| Travel | $2,460.20 | 27% |

| Mortgage | $2,192.80 | 24% |

| Groceries | $864.61 | 10% |

| Utilities | $696.35 | 8% |

| Everything Else | $2,826.98 | 31% |

| Total | $9,040.94 | 100% |

Strip out travel and May was ~$6.6K — above my $5K target. Mortgage and utilities are the fixed core. The rest — groceries, dining, fitness — ran a bit full but nothing alarming. No single blow-up.

The travel charge is the credit card tail from April's trip. Planned, not creep.

Reflections

-

The $235K finally moved. ~$71K out of SNSXX this month: ~$44K into VT (285 shares split across taxable and backdoor Roth IRA), ~$16K to clear the M1 loan. The decision doc said $5K/month DCA — I did it in two days once I stopped talking about it. Cash still runs about 3 points above the 7% target. More to come. The expensive non-decision era is over.

-

M1 at $0. The margin loan was $15.9K heading into May. The plan said ~3 months to clear it. Done in one. Clean balance sheet on the liability side now — just the mortgage.

-

The paycheck that doubled. ESPP capped on 05/08. The 05/22 check showed up as ~$4.7K take-home vs the previous $2.3K. Same job, same gross. The automation is starting to pay out — ~$5K/month through December landing in checking.

-

45.4% there. Seven months of slow. Since crossing $2M last October, net worth is up ~$270K. Slow is the point.

Next up: continuing the bond leg of the rebalance, letting the Phase 2 DCA automation run, and watching whether the cash position drifts toward 7% on its own.

Your turn. When you set a target allocation, do you rebalance mechanically (drift hits a threshold, you act), or more intuitively (something feels off, you look and then decide)? I landed on targets partly through analysis and partly through gut. Curious how others think about it — drop a comment.

Join the Quest

This blog is my public commitment to the grind from $2M to $5M. If you're a high earner tired of the corporate hamster wheel and want to see the real numbers behind the exit, subscribe and follow along. Let's figure this out together.

Member discussion